The following is a handout from Tim Agnew - Masthead Venture Partners - given to the Taxation Committee relating to the Seed Capital Tax Credit.

....Exceptional work Tim - Thank You!

....Legislative Alert #1 regarding L.D. 1666 is posted at http://www.techmaine.com/LD1666

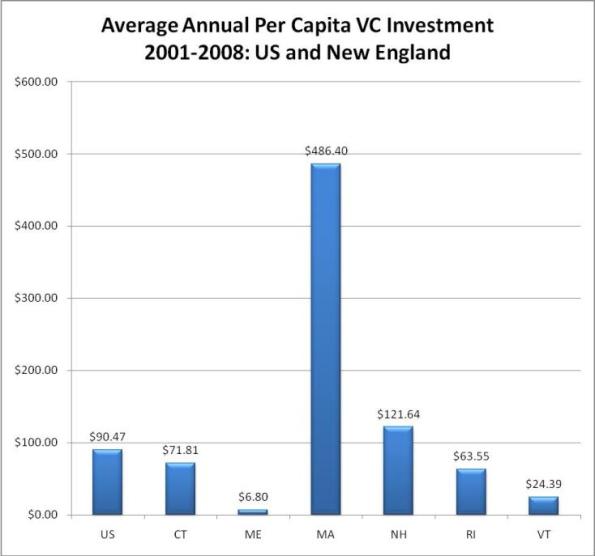

Source: PricewaterhouseCoopers/National Venture Capital Association MoneyTree Report

Venture capital differs from loans in that it is patient capital (typically no returns for many years) and high risk capital with the potential for a complete loss. Banks make loans to businesses that demonstrate the ability to make regular payments of interest and principal based on their past financial record. Venture capital investors place capital at risk in anticipation of the future prospects of a business. Lenders expect minimal losses on their loans, and generally their profit is limited to the interest on the loan. Venture investors, particularly in early stage businesses, accept a much higher risk of loss in exchange for the hope for high returns on their investment. Venture investors seek investments where the risk of loss is outweighed by the potential return. If the risk is too high in relation to the potential return, the investor will not make the investment.

Businesses that are candidates for venture capital must have the potential for rapid growth, and generally are technology-based businesses that pay higher wages than more traditional businesses. Lack of access to capital impairs the ability of these high growth small businesses to continue to grow, and jeopardizes their very survival. It also jeopardizes the investment the State may have made in those businesses through the Maine Technology Institute and the Small Enterprise Growth Fund.

LD 1666 addresses the problem in two ways. First, it encourages investors to make eligible investments by reducing the risk side of the risk-reward equation. Increasing the Seed Capital Tax Credit from 40% to 60% reduces the investor’s downside risk and makes the investment more attractive. The result is to make it more likely that high-potential enterprises will be able to raise the venture capital they need.

The second initiative would dramatically expand the potential pool of investors by making the Seed Capital Tax Credit refundable. A refundable credit would allow venture investors that are not currently Maine taxpayers to take advantage of the Seed Capital Tax Credit. This would make investing in Maine entrepreneurs far more attractive to a huge pool of out-of-state investors.

The result of these proposals would be more investment in Maine businesses, which would use the money to hire staff, buy goods and services, bring products to market, increase sales and attract additional capital. This would have a multiplier effect and produce future tax revenues that should more than offset the cost to the State.

2. Comparison of 40% vs. 60% Seed Capital Tax Credit:

Simply stated, the typical investor under the proposed legislation would, for each $100,000 invested, get a return from the Bureau of Revenue Services of $60,000 over four years rather than $40,000 over four years. On a successful investment, the return to the investor is enhanced. On an unsuccessful investment, the loss suffered by the investor is reduced. The primary attractions to the investor are (1) the downside protection of part of their investment, and (2) getting a partial return of the investment during the first four years of an investment while waiting to find out whether the investment will be successful.

A typical example might be the investor who invests $100,000 in a company initially, followed by additional investments of $50,000 in years 2 and 3. In year 10, the company is sold. The after-tax[1] gain or loss to the investor is shown below based on three scenarios: a success with a $1,000,000 return, a breakeven investment with a $200,000 return or a complete loss:

Source: PricewaterhouseCoopers/National Venture Capital Association MoneyTree Report

Venture capital differs from loans in that it is patient capital (typically no returns for many years) and high risk capital with the potential for a complete loss. Banks make loans to businesses that demonstrate the ability to make regular payments of interest and principal based on their past financial record. Venture capital investors place capital at risk in anticipation of the future prospects of a business. Lenders expect minimal losses on their loans, and generally their profit is limited to the interest on the loan. Venture investors, particularly in early stage businesses, accept a much higher risk of loss in exchange for the hope for high returns on their investment. Venture investors seek investments where the risk of loss is outweighed by the potential return. If the risk is too high in relation to the potential return, the investor will not make the investment.

Businesses that are candidates for venture capital must have the potential for rapid growth, and generally are technology-based businesses that pay higher wages than more traditional businesses. Lack of access to capital impairs the ability of these high growth small businesses to continue to grow, and jeopardizes their very survival. It also jeopardizes the investment the State may have made in those businesses through the Maine Technology Institute and the Small Enterprise Growth Fund.

LD 1666 addresses the problem in two ways. First, it encourages investors to make eligible investments by reducing the risk side of the risk-reward equation. Increasing the Seed Capital Tax Credit from 40% to 60% reduces the investor’s downside risk and makes the investment more attractive. The result is to make it more likely that high-potential enterprises will be able to raise the venture capital they need.

The second initiative would dramatically expand the potential pool of investors by making the Seed Capital Tax Credit refundable. A refundable credit would allow venture investors that are not currently Maine taxpayers to take advantage of the Seed Capital Tax Credit. This would make investing in Maine entrepreneurs far more attractive to a huge pool of out-of-state investors.

The result of these proposals would be more investment in Maine businesses, which would use the money to hire staff, buy goods and services, bring products to market, increase sales and attract additional capital. This would have a multiplier effect and produce future tax revenues that should more than offset the cost to the State.

2. Comparison of 40% vs. 60% Seed Capital Tax Credit:

Simply stated, the typical investor under the proposed legislation would, for each $100,000 invested, get a return from the Bureau of Revenue Services of $60,000 over four years rather than $40,000 over four years. On a successful investment, the return to the investor is enhanced. On an unsuccessful investment, the loss suffered by the investor is reduced. The primary attractions to the investor are (1) the downside protection of part of their investment, and (2) getting a partial return of the investment during the first four years of an investment while waiting to find out whether the investment will be successful.

A typical example might be the investor who invests $100,000 in a company initially, followed by additional investments of $50,000 in years 2 and 3. In year 10, the company is sold. The after-tax[1] gain or loss to the investor is shown below based on three scenarios: a success with a $1,000,000 return, a breakeven investment with a $200,000 return or a complete loss:

$1 Million Return $200,000 Breakeven Total Loss After-tax gain/loss with 40% Credit: $752,000 $52,000 -$108,000 After-tax gain/loss with 60% Credit: $778,000 $78,000 -$82,000 After-tax gain/loss Assuming no Credit: $700,000 $0 -$160,000

3. How Much of the Investor’s Risk is Eliminated by the Credit: The question was asked what the actual loss to an investor is if she gets the 60% credit and is able to write off the investment as a loss. On an after tax basis, the Seed Capital Tax Credit is worth about $78,000 on a $200,000 investment. The write-off results in a tax benefit of about $40,000, so the net loss is $82,000. In other words, the 60% Seed Capital Tax Credit covers only 59% of the loss on an after-tax basis. This is much less than the 80-85% number we speculated on at the Public Hearing. The 40% credit covers 46% of the loss on a complete failure of an investment. The investor continues to have a significant share of the downside risk of loss and will factor that risk into investment decisions, yet has far more incentive to make an investment than without the Seed Capital Tax Credit. 4. Comparison of Direct Investment Option vs. Expanded Tax Credit: Another question was whether it would make more sense to invest the money directly rather than expanding the Seed Capital Tax Credit. As an example, $600,000 that would otherwise go to investors under the Seed Capital Tax Credit Program could be invested directly into businesses by the Small Enterprise Growth Board (SEGB), the State’s publicly funded venture capital fund. This suggestion has the advantage of capturing all of the returns on successful investments for reinvestment by the SEGB. However, it has two primary weaknesses. First, the direct investment model would forego the additional $400,000 in private investment capital that would need to be invested to obtain the $600,000 in Seed Capital Tax Credits. In other words, available investment dollars would be reduced by 40%. Second, it would result in fewer prospective investors for Maine entrepreneurs. The Seed Capital Tax Credit attracts investors to look at Maine businesses. Without access to the credit, the attractiveness of Maine businesses would be lessened and the amount of venture capital invested in the State would decline. As indicated on the attached table of venture capital investment, Maine already suffers from low venture capital activity. We need to attract more active investors. LD 1666 would accomplish that goal. 5. Fairness to In-State Investors: As currently drafted, LD 1666 would allow out-of-state investors to apply for a refund of the full amount of the Seed Capital Tax Credit amount due to them. In-state investors would continue to be limited to reducing their current State tax liability by no more than 50%. While the amount of the credit available would be the same to in- and out-of-state investors, there would arguably be an inequity in making it refundable for out-of-state investors but not for residents. This concern could be addressed by making the credit fully refundable for all investors for investments made after the effective date of the Bill, which should be amended to be not sooner than 90 days after the end of this Legislative Session. 6. Fiscal Impact: In 2009, the Seed Capital Tax Credit Program had the lowest volume of usage in 17 years. As a result, the cost to the State is below projections and below the estimates used in crafting the State Budget. The purpose of LD 1666 is to increase venture capital investment in the State and that will eventually result in increased usage of the Seed Capital Tax Credit. Assuming the effective date of the increase in the Seed Capital Tax Credit is for investments made after the effective date of the Bill, there should be no increase in cost during this Biennium. The legislation proposes holding the credit percentage the same in the first two years, then increasing in the third and fourth years. The result is to defer any increase in cost to the State. It is also important to recognize that the investment takes place before the investor can apply for the Seed Capital Tax Credit, so the benefits of the investment in the form of jobs and economic growth are in place before the Tax Credit is paid out to the investor.[1] Assuming 35% federal tax bracket, Section 1202 stock (7.5% federal rate on capital gains, 15% on losses) and 5% state tax rate.